Disclaimer

Nothing discussed/written should be considered as investment advice. Please do your own research or speak to a financial advisor before putting a dime of your money into these crazy markets. In other words, if you buy something I bought, you deserve to lose your money.

The only reason why I am making my portfolio public because it provides accountability to me. Some or all the analysis I provide could be from the top of my head and should not be considered accurate.

My investing goal is simple; to try to manage risk while being fully invested without market timing. Howard Marks said it best, “even though we can’t predict, we can prepare.”

All my references to the Market are only for the US Market.

Performance

During Q1 of 2023 my portfolio returned 0.79% compared to 7.5% for the S&P 500 (with dividends reinvested).

The table below is a breakdown of my portfolio at the end of Q1 2023. What you see below where my entire net worth, excluding my home, is allocated. Lastly, my 401k is 100% invested in a Small Cap Value Fund.

| Company | % |

| AIMFF | 3.7% |

| AVDE | 0.2% |

| AVDV | 0.7% |

| AVES | 0.9% |

| AVIV | 0.5% |

| AVSC | 0.0% |

| AVUV | 0.6% |

| BAC | 2.7% |

| BRK.B | 14.5% |

| BSBK | 0.1% |

| BTI | 1.5% |

| BWFG | 0.0% |

| C | 1.4% |

| CFSB | 0.1% |

| CLBK | 0.0% |

| COF | 1.0% |

| CSV | 7.2% |

| CULL | 0.1% |

| DFEV | 1.0% |

| DFIC | 0.6% |

| DFIV | 0.6% |

| DFSV | 0.5% |

| DISV | 0.6% |

| EPD | 2.8% |

| EWUS | 0.0% |

| FFBW | 0.3% |

| FPI | 0.0% |

| FSEA | 0.1% |

| GVAL | 2.6% |

| HII | 0.6% |

| INTC | 0.8% |

| IVAL | 0.3% |

| LAND | 0.0% |

| LMT | 0.5% |

| MKL | 4.7% |

| MMP | 3.9% |

| MU | 8.1% |

| NECB | 0.2% |

| PBBK | 0.1% |

| PREKF | 0.8% |

| TCBC | 0.1% |

| TCBS | 0.1% |

| USB | 0.5% |

| WMPN | 0.1% |

| T Bills | 8.3% |

| Gold | 3.3% |

| Platinum | 0.8% |

| Farmland | 4.0% |

| I Bonds | 7.4% |

| Cash | 1.8% |

| 401k | 9.2% |

Below is a breakdown by category:

| Bonds | 7.38% |

| Cash | 1.80% |

| Conglomerate | 14.49% |

| Defense | 1.09% |

| Financials | 7.00% |

| Funeral | 7.21% |

| Insurance | 4.74% |

| International | 8.01% |

| Manager | 3.71% |

| Oil/Gas | 7.50% |

| Precious Metals | 4.06% |

| Real Estate | 4.01% |

| Semiconductor | 8.87% |

| Small Cap Value | 10.31% |

| T Bills | 8.29% |

| Tobacco | 1.51% |

Commentary

The only change I made to the portfolio was I started a small position in Capital One. My buy price was essentially at tangible book value. I initiated the position during the bank collapse SVB Bank.

In terms of going forward I don’t have any view. I know the Market is very bearish and I can understand why. I still think the economy is doing well; everywhere I go I see people spending money. It is concerning that it looks like white collar jobs are being eliminated and I don’t see how in the long term this doesn’t have a negative impact on the economy 6-12 months from now.

With gold at around $2,000 it is tempting to sell my gold and buy Treasury Bills with the money but if the economy doesn’t do well then gold may have more room to run. Also, I don’t need to sell the gold which means I’ll let it run.

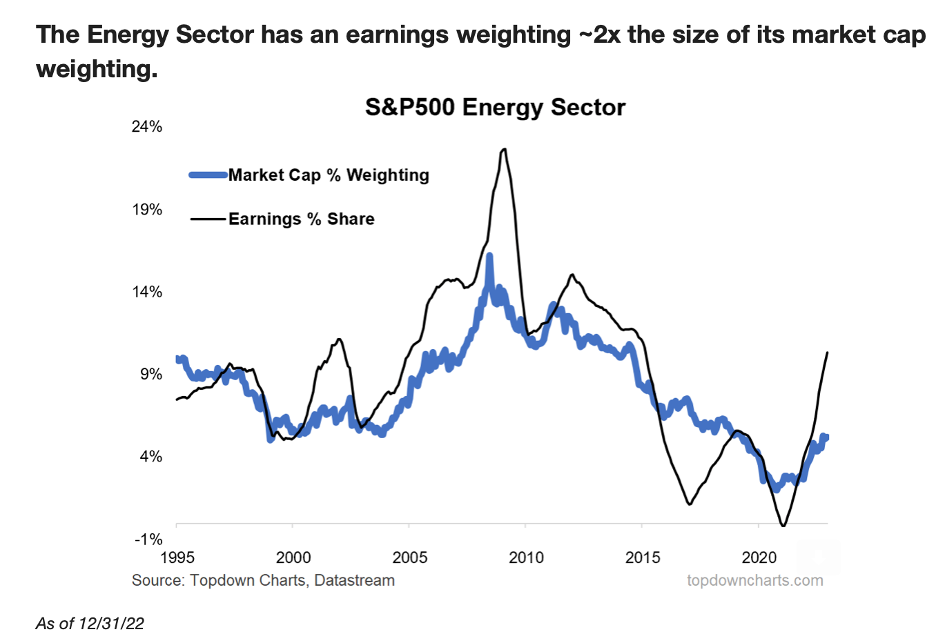

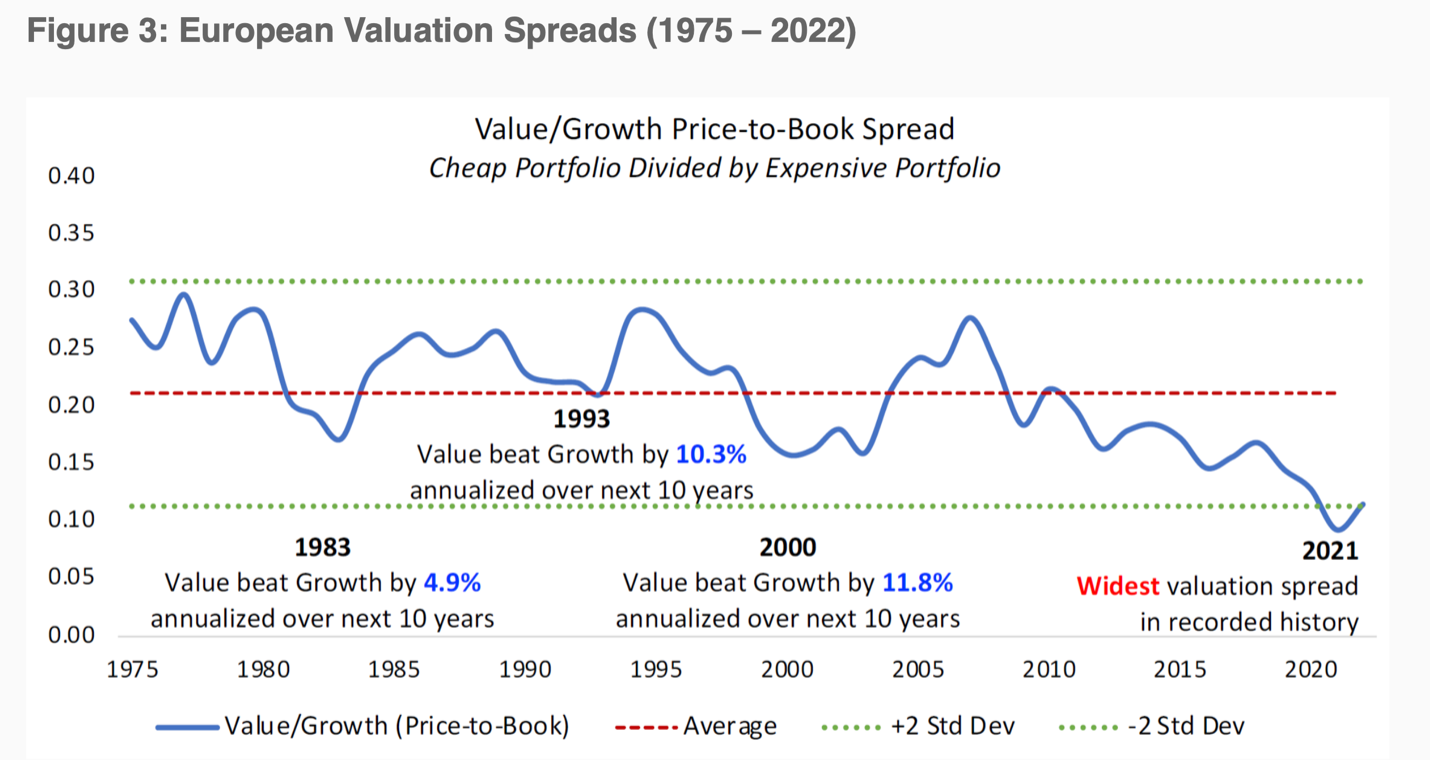

Below are charts and quotes I enjoyed during Q1 this year:

“At this juncture, you can either invest based on a belief in business cycles and normalization or invest based on faith that the economy can be successfully managed forever.” Source: Q4 letter from https://www.palmvalleycapital.com/fundletter

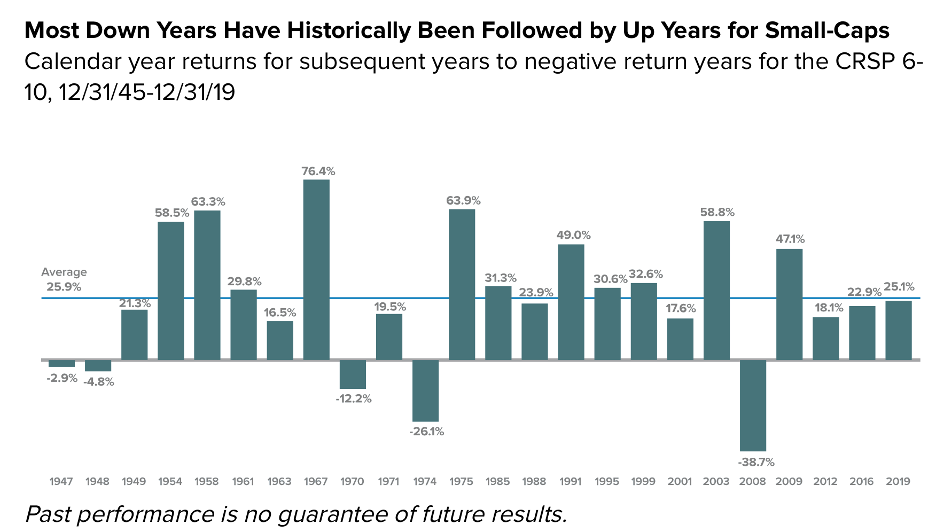

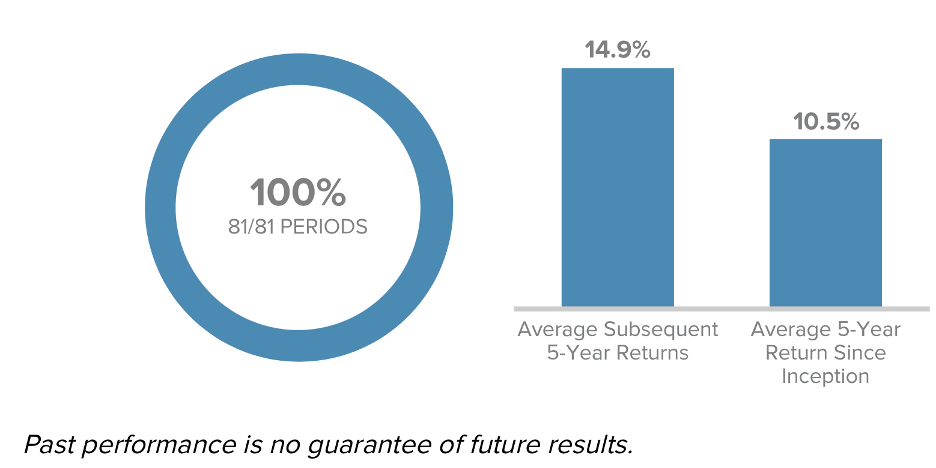

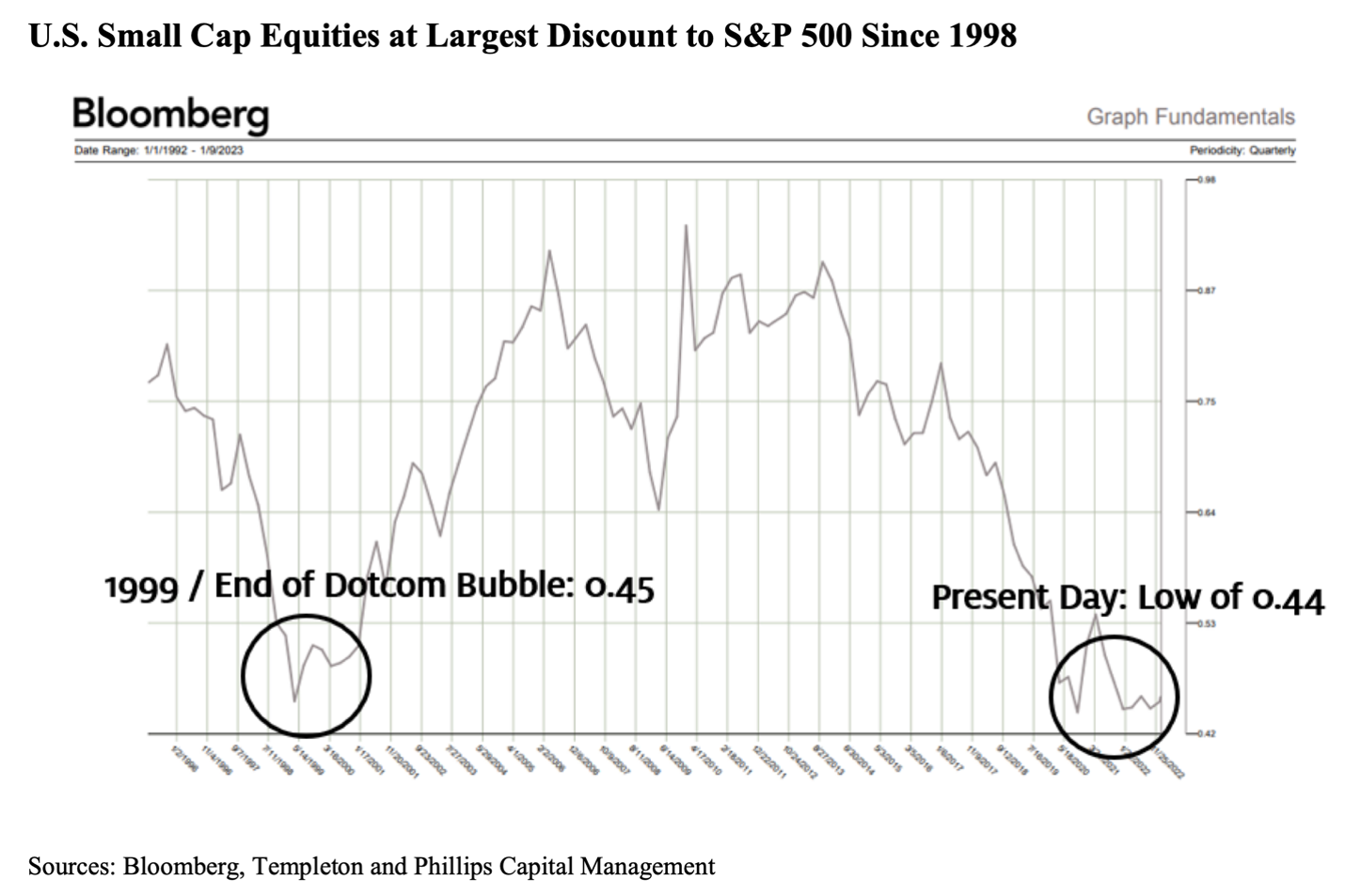

“In our view, these historical patterns not only suggest a low probability of loss for small-caps over longer-term periods of at least three years, but they also imply that the opportunity cost of waiting or trying to time a bottom—whether for the market or the economy—may be high. So while no one can predict future outcomes for the markets or the economy, we can carefully examine small-caps’ past performance patterns in a way that helps us make sense of the present as we prepare for the uncertain days ahead.”https://www.royceinvest.com/insights/small-cap-recap#:~:text=Small%2DCap%20Value%20and%20Quality,%25%20in%204Q22%20versus%204.1%25

Source: https://www.gmo.com/americas/research-library/memo-to-the-investment-committee-a-hidden-gem/

“Today (January 30, 2023), deep value companies in Europe can be purchased at around 5x EV/EBITDA and 0.8x Price/Book, based on data from S&P Capital IQ. If firms in that category prove to be more resilient than the pessimistic expectations embedded in their prices would imply, they could significantly benefit from multiple expansion over time and still avoid looking expensive. And while waiting for the fruits of mean reversion, we believe investors in European deep value companies can benefit from cash distributions in the form of dividend yields around 4%, share buybacks, and deleveraging.”

Source: https://mailchi.mp/verdadcap/after-the-darkest-hour-comes-the-dawn?e=e1c5773556

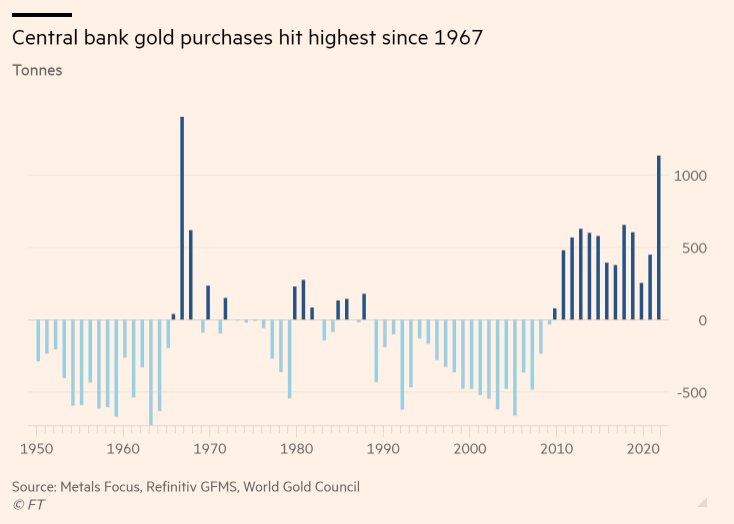

“Annual gold demand increased 18 per cent last year to 4,741 tonnes, the largest amount since 2011, driven by a 55-year high in central bank purchases, according to the World Gold Council, an industry-backed group.”

Source: https://www.ft.com/content/ef6ed550-422a-4540-a8af-41ff2ac30e67

“[Meanwhile] stocks are caught between a rock and hard place. Strong nominal growth (either via inflation or real gains) will force the Fed to hold rates higher and tighten financial conditions further…. A worst scenario is an outright recession, with falling earnings, sentiment, and growth.”

Source: https://thelastbearstanding.substack.com/p/has-the-rally-peaked

“As of this writing, the S&P 500 is at $3,850 and earnings estimates for 2022 are around $200. This means that the average stock in this index is trading at approximately 19x earnings, which is a high number, especially in the current rising-interest-rate environment, but not insane (the historical average is around 15x).

Currently, profit margins are 11.5%, down from 12.1%, which was an all-time high just a few months ago. Over the last 75 years, corporate profit margins have averaged about 7.1%. Over the last 30 years profit margins were 8.2%. In the 1980s, profits averaged 5.3%, in the 1990s 5.7%, and in the first decade of the century they were 7.9%. If profit margins settle at the level of the past decade, at 10.2%, then the market will be trading at about 22 times earnings. If margins return to their former levels, we may find that the earnings power of the S&P 500 is $91-$143 per share, or in other words, stocks are trading 27-42 times earnings.”

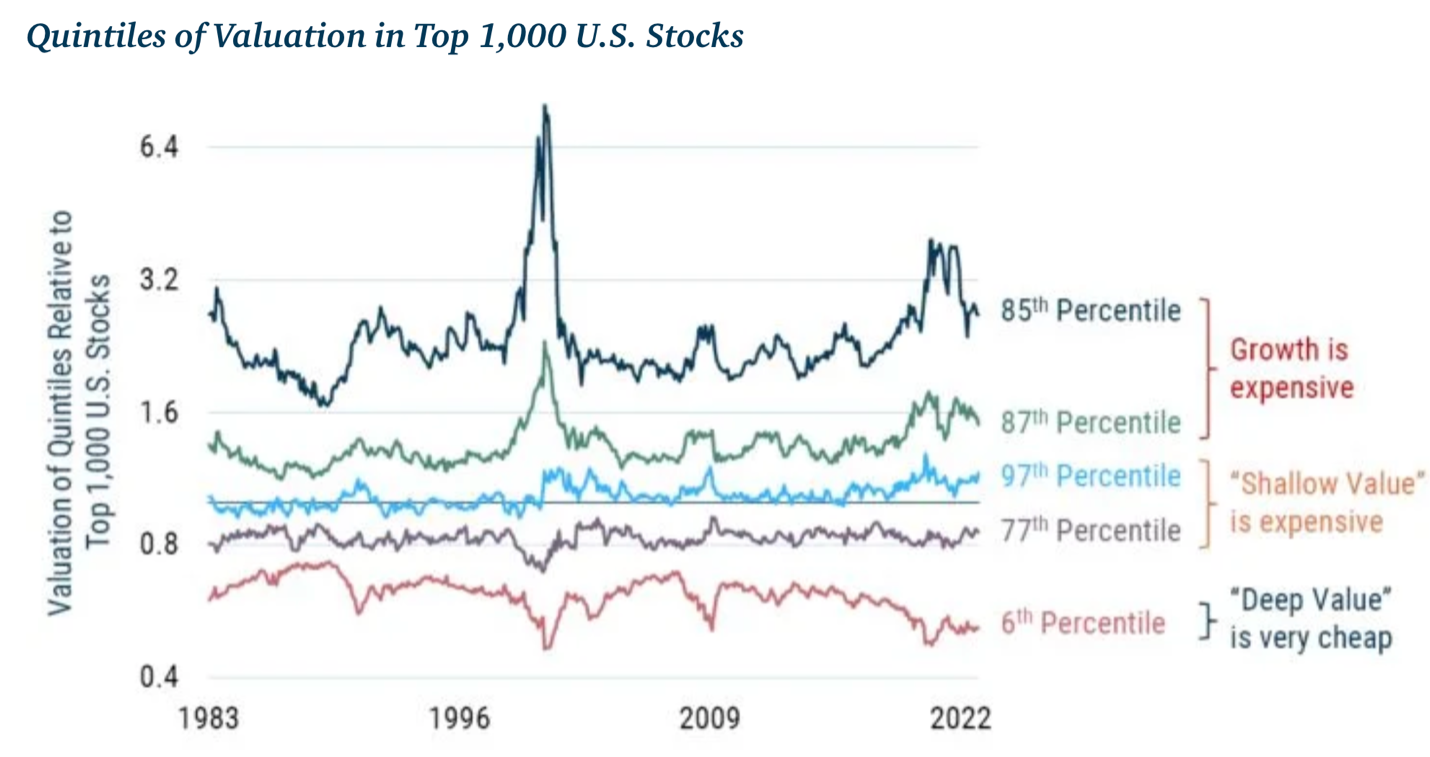

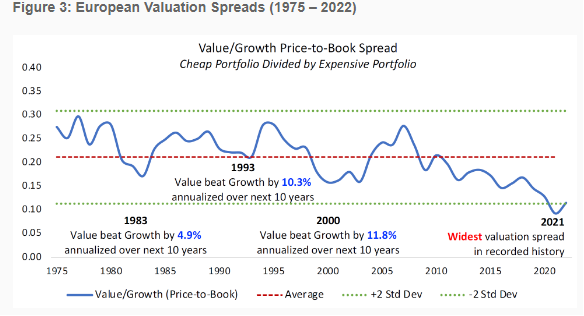

“For value investors, the above findings are good news, as the largest historical drawdown for the value premium from November 2016 through October 2020 led to a dramatic widening of the book-to-market spread between value and growth stocks. Even with the strong performance of the value premium since then, the spread is still much wider than its historical average and much wider than it was when Eugene Fama and Kenneth French published their famous study “The Cross-Section of Expected Stock Returns” in 1992. Thus, the expectation is that the value premium will be larger than its historical average.

Source: https://alphaarchitect.com/2023/02/dark-winter-value-stocks/

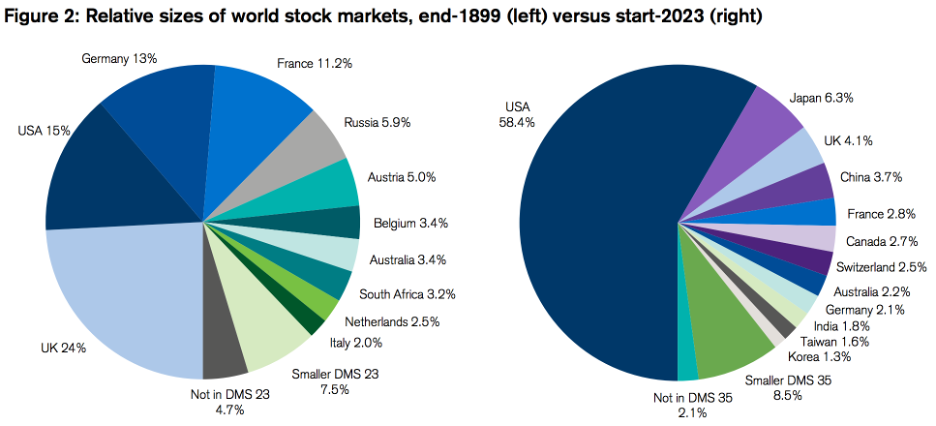

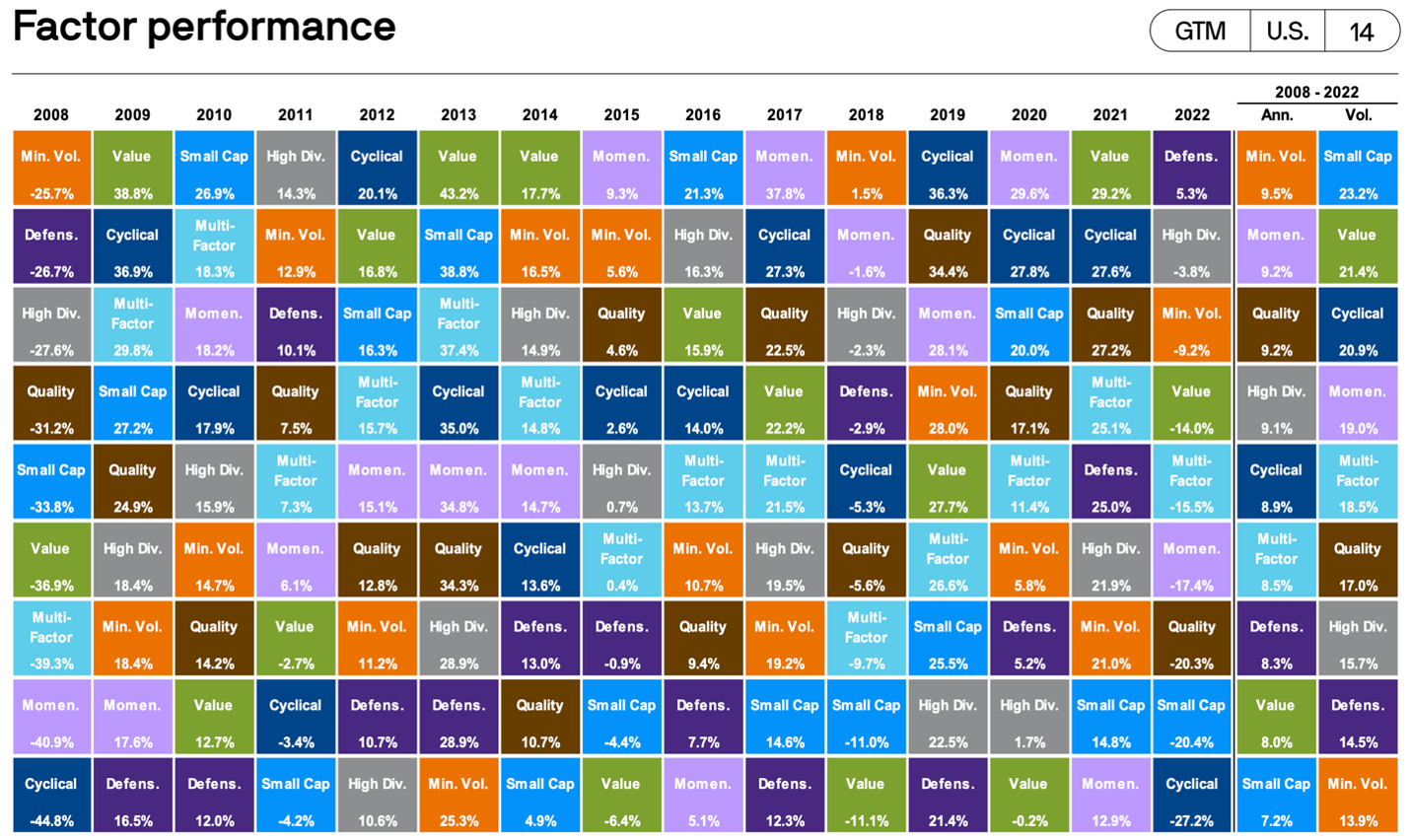

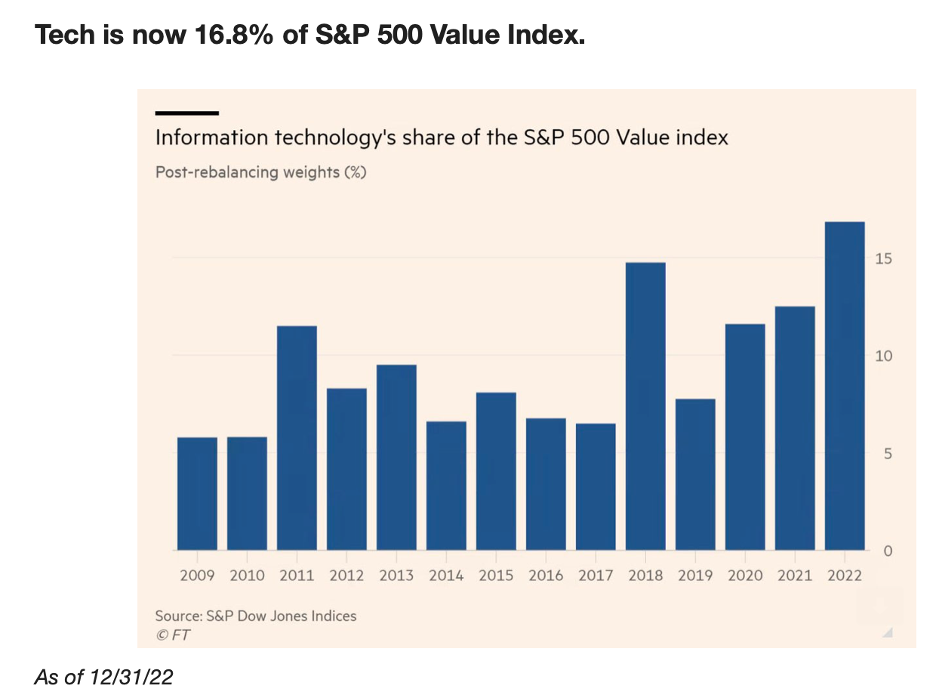

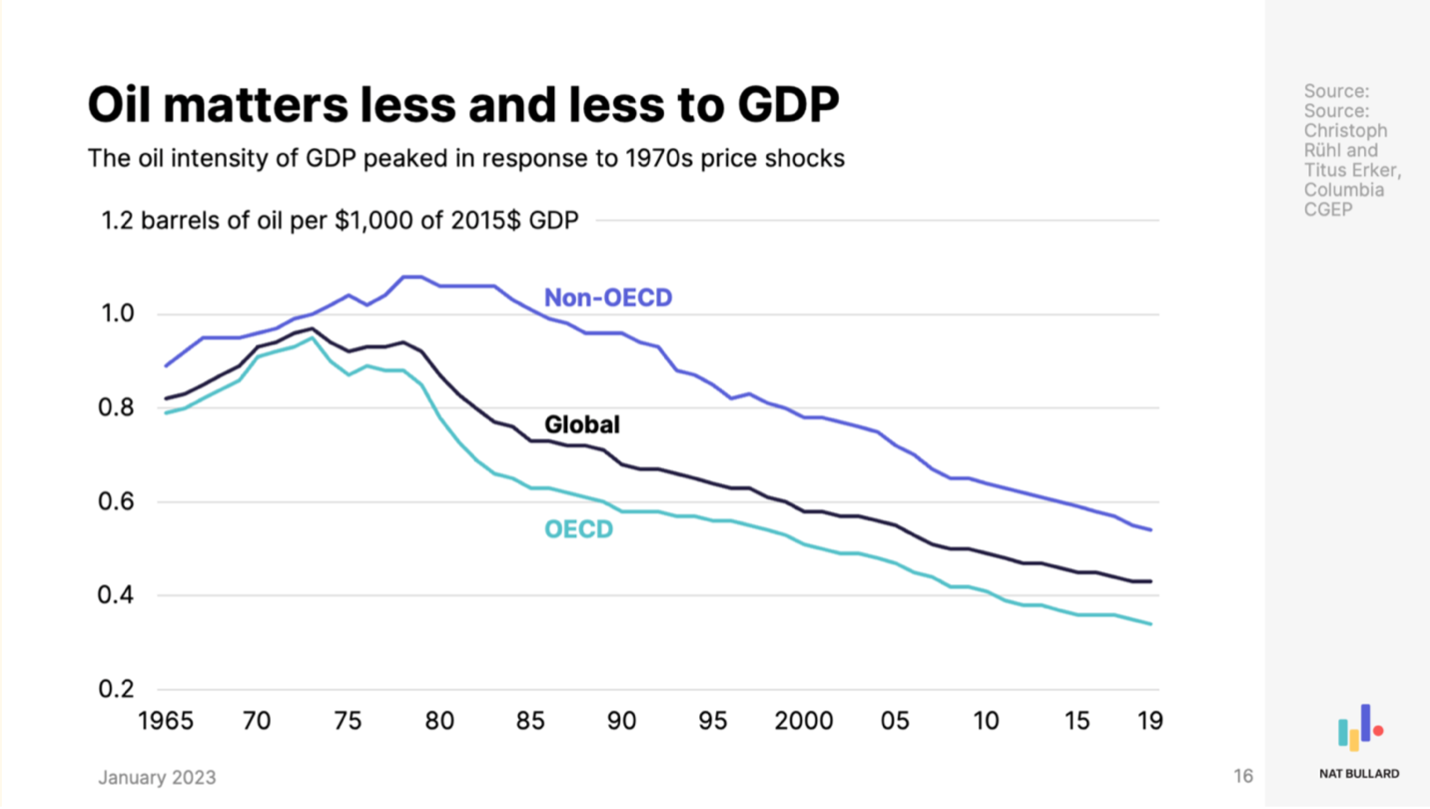

Source: https://www.nathanielbullard.com/presentations

“Further, we see no reason that smaller companies should fare as poorly this decade as they did in the past one. We would argue that the current P/E discount for smaller stocks suggests a reversal is more likely than a continuation, which should benefit Oakmark Select more than Oakmark.”

Bill Nygren https://oakmark.com/news-insights/why-we-still-believe-in-concentrated-investing/

“Going forward: in prior research, we’ve laid out what we think is a reasonable path to equilibrium. In a nutshell, we see it looking something like this.

- To get 2% inflation, you need a deceleration in wage growth from the prior 5% to about 2.5%.

- To reduce wage inflation, you need to cut nominal spending and income growth in half to 3-5% and raise the unemployment rate by 2% or more.

- To raise the unemployment rate, you need to drive nominal GDP growth materially below wage growth and compress profit margins enough to produce about a 20% decline in earnings.

- After that, you need to hold short-term interest rates steady for about 18 months, until 2.5% wage growth, 2% inflation, and 2% real growth are sustainably achieved.

- Then cut short-term interest rates to about 1% below then-existing bond yields.”